When we talk of personal insurances, one question which arises in the minds of retail customers is what are the insurance policies one must have? If one cannot afford to buy all of those insurance products, how to prioritise them. In other words, with so many different Insurance products being available in the market, which product is essential for the retail customer? Which product should be purchased immediately and which one can be deferred to a later date, keeping in mind the premium affordability? What is the hierarchy of Insurance products for an individual?

Legally Mandated Insurances:

There are certain Insurances which are mandated by law and known as Compulsory or Mandatory Insurances. The purpose of these laws is to ensure that if there is any third party suffering losses due to an individual, that Individual is responsible for compensating those losses, through the Insurance mechanism.

The best example for such an insurance is Third Party Insurance for Motor Vehicles. As per Motor Vehicle Act, no person shall use a motor vehicle in a public place, unless there is a valid third party liability Insurance in place. This means that no individual can use a scooter or car or any other motor vehicle in any public place without buying an insurance which provides for compensation to third parties, in case the vehicle causes physical injury or property damage to third parties. Using the vehicle without such Insurance is punishable with fine or imprisonment or both. These kinds of mandatory Insurances should occupy the first place in the list of Insurance products to purchase.

Non-Mandatory Insurances-Criterion for Prioritising:

In respect of non-mandatory insurances, there are certain critical parameters which must be analysed while deciding on the Hierarchy of Insurance Needs or priority of Insurance Products.

- Firstly, What is the size of loss that could be compensated under the product? Is it large like property loss in a fire or small like a pedal cycle loss due to theft? Insuring the house building against fire should be higher priority than insurance of a pedal cycle against theft.

- Secondly, What is the probability of loss i.e chance of occurrence of loss under the product? Is it high like hospitalisation claim under health insurance policy or low like a burglary loss under a burglary policy?

- What is the premium outgo? Is it high like under a Health Insurance policy or low like under a Personal Accident Policy? If the premium outgo is high and is unaffordable at a given life stage, customer has no option but to defer the purchase till his affordability level increases.

Of course, one should be mindful that during the period when the policy is not purchased, the customer has to carry the risk himself, which is not advisable.

One needs to carefully analyse the products in light of above aspects and come out with a list of products in the order of priority for purchase.

Hierarchy of Insurance Products:

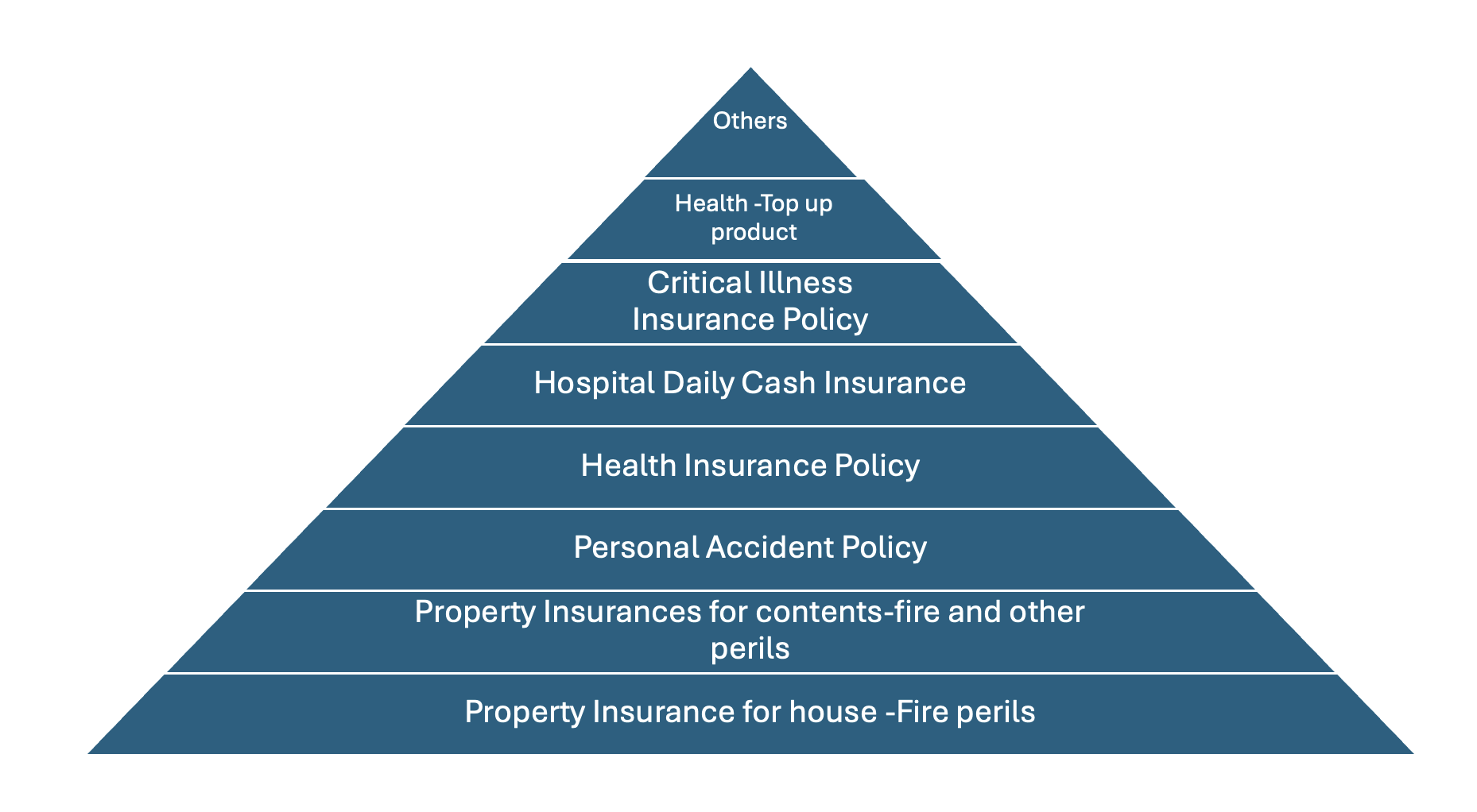

In my view, for a retail or individual customer, the insurances to be purchased for complete protection, in the order for priority, excluding the mandatory insurances, should be as follows:

- Property Insurance for house against fire perils

- Property Insurances for contents of the house against fire and other perils

- Personal Accident Policy

- Health Insurance Policy

- Hospital Daily Cash Insurance

- Critical Illness Insurance Policy

- Health Insurance Policy-Top up product

- Other Insurances like Cyber Safe, Pet Insurance, Event Cancellation and others.

Besides these products, Overseas Travel Insurance is a must, as and when the person is travelling abroad. The cost of Travel Insurance should be considered more as a part of travel expenses and has to be necessarily incurred, as any medical emergency abroad can prove to be a major loss due to medical costs abroad.

The reasons I have considered for arriving at the hierarchy are as explained below:

- The property damages due to fire could lead to large damages and can have long term impact on the customers’ finances. Similarly, death of an earning person in an accident can throw the family of the person into a long period of financial difficulty. Also, the premium rates for these policies are relatively low. Hence, I consider them on the top of the Hierarchy of Insurance purchase needs.

- Health related insurance policies are very critical for the financial stability, as the sickness probabilities are high. However, the probability of large losses are less than the probability of smaller losses. Many of the retail customers might be able to withstand the financial pressures of smaller losses. Hence, this product is placed after property damage covers in terms of priority. (Of course, the terms, large and small are used relatively-no financial loss can be considered as small for an individual)

- Hospital daily cash, Critical Illness, top-up products help in enhancing the health insurance coverage, by providing additional protection. These products are not the core covers. Hence, they are placed after the core health Insurance cover.

- The other Insurances placed at the end of the hierarchy does not mean that these policies are unimportant. Losses like Cyber risk losses are increasing both in probabilities and magnitudes. It is only relatively, that they occupy a lower need.

Of course, depending on the Individuals risk retaining capacity and premium paying affordability, the order of priority may change from what I have stated here.

Ideally, each and every family needs to have these insurances in place, for a comprehensive coverage leading to stress free life. Where you find it difficult to pay premium for all of them, you should atleast consider covering property Insurances, Personal Accident Insurance and Health Insurance for smaller sum Insured. The same can be widened as and when it becomes feasible.

- The above list excludes mandatory Insurance Products

- Besides these products, Overseas Travel Insurance is a must, as and when the person is travelling abroad. The cost of Travel Insurance should be considered as part of travel expenses and has to be necessarily incurred, as any medical emergency abroad can prove to be a major loss due to medical costs abroad.